Risk Scoring Models

How Credit Pulse scores risk and how to interpret each score in your workflow.

Our scoring models are built using machine learning trained on thousands of companies. They analyze real-world outcomes such as bankruptcies and payment behavior to predict future risk.

Each score ranges from 0 to 100 and is relative, meaning it ranks a company compared to others in our dataset.

High Risk = 0 - 30

Moderate Risk = 31-70

Low Risk = 71-100

Scoring Overview

Each score answers a different question:

Pulse Score → Overall risk

Health Score → Likelihood of failure

Payment Score → Likelihood of paying late

Used together, they give you a more complete picture:

High Health + Low Payment = stable but slow payer

Low Health + High Payment = paying now, but risk ahead

Low across all = high-risk account

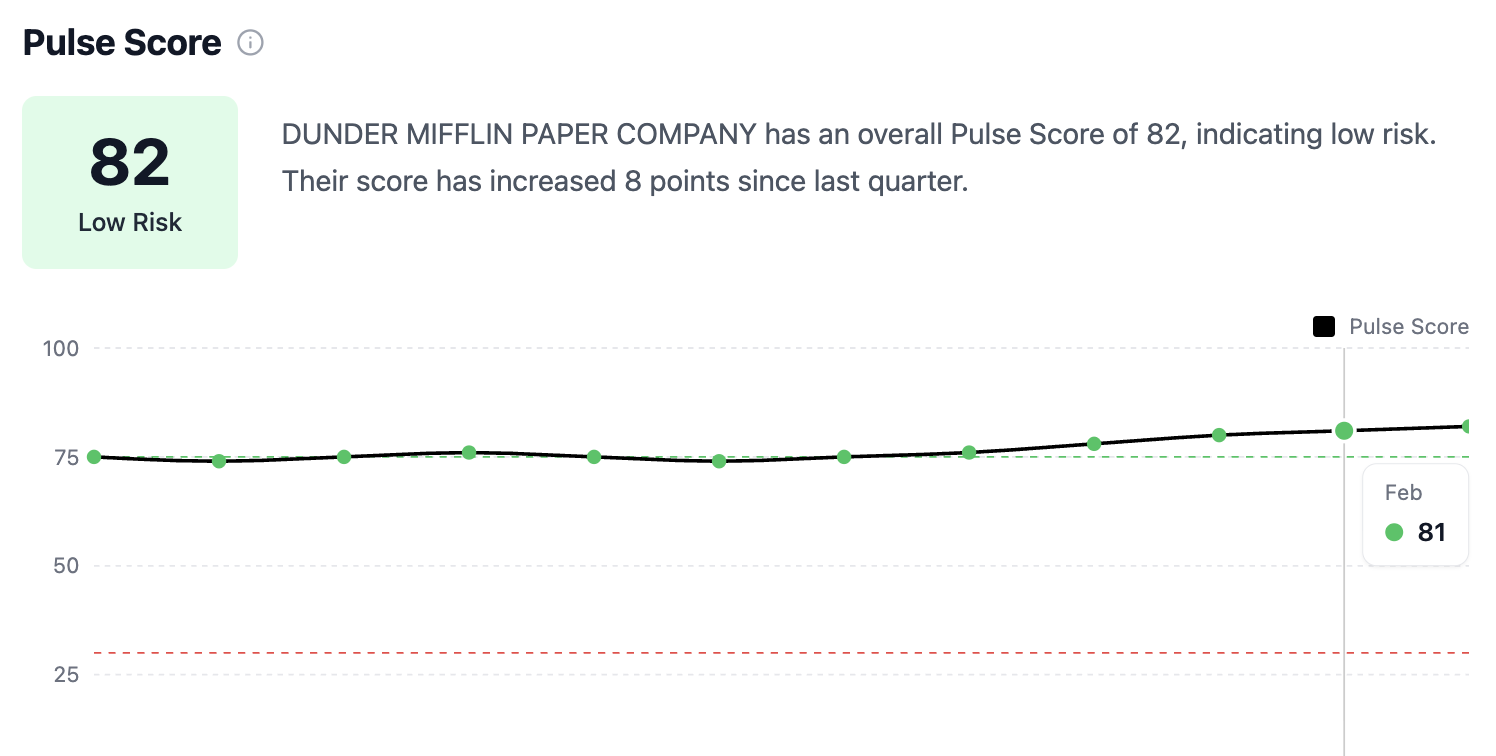

Pulse Score

The Pulse Score is our highest-level risk indicator. It gives you a single, comprehensive view of a company’s overall risk.

It combines multiple data sources and signals into one score so you can make quick decisions without digging through fragmented data.

What it considers:

Bankruptcy risk signals

Payment behavior

Company stability and activity

Financial and operational indicators

Alternative data (news, hiring trends, etc.)

How to use it:

Use as your primary decisioning score

Ideal for quick approvals, declines, or prioritization

Best starting point before diving deeper into details

Think of Pulse Score as your “should I extend credit?” shortcut.

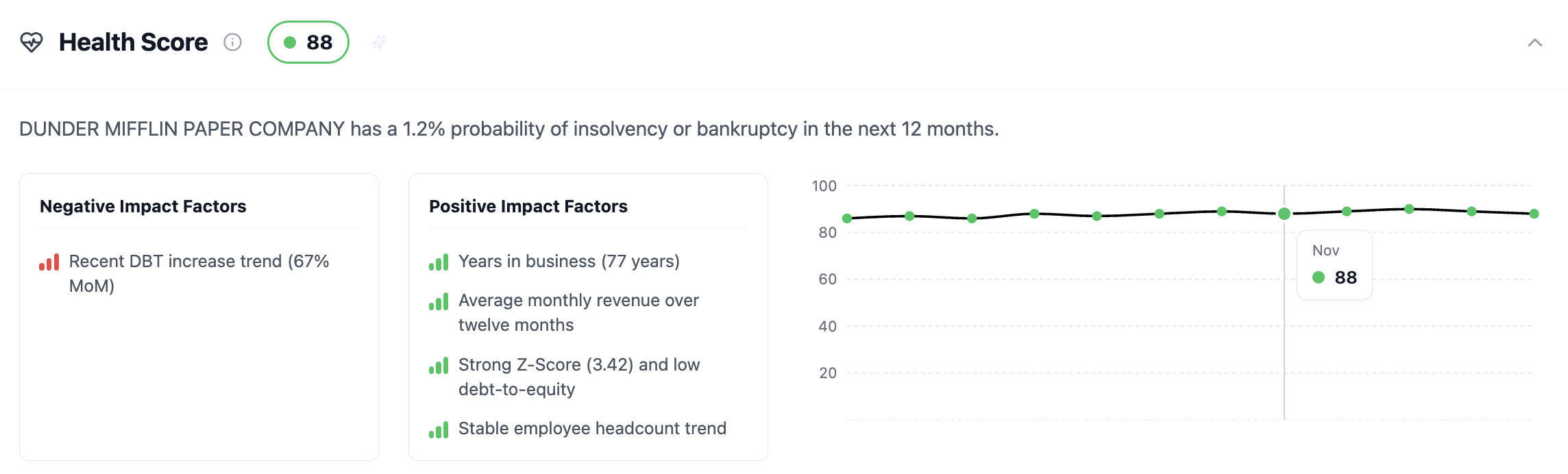

Health Score

The Health Score focuses specifically on financial stability and bankruptcy risk.

It estimates the likelihood that a company may become insolvent within the next 12 months.

What it considers:

Financial trends and ratios

Company longevity

Revenue and size indicators

Structural risk signals

Stability metrics over time

What you’ll see:

Probability of bankruptcy or insolvency

Positive and negative contributing factors

Trend over time

How to use it:

Validate long-term risk exposure

Monitor existing customers for deterioration

Identify early warning signs before issues surface

Think of Health Score as your “will they survive?” signal.

Payment Score

The Payment Score predicts how likely a company is to pay late or miss payments.

It focuses on short-term behavior rather than long-term viability.

What it considers:

Trade payment data

Days beyond terms (DBT)

Changes in payment patterns

Industry payment benchmarks

What you’ll see:

Probability of late payment

Payment trend over time

Key drivers impacting behavior

How to use it:

Set credit terms and limits

Prioritize collections

Flag accounts that may become slow payers

Think of Payment Score as your “will they pay you on time?” signal.

Prediction Accuracy

Traditional credit scores rely on static financials and lagging data. By the time risk shows up, it’s often too late.

Our models combine real-time signals, broader datasets, and machine learning trained on actual outcomes to surface risk earlier and more reliably.

What's Different

Beyond financials: We incorporate payment behavior, operational signals, news, and workforce trends.

Real-time vs. point-in-time: Traditional scores update periodically. Our models continuously evaluate changes, so you see risk as it develops, not months later.

Built for private companies: Our model works with or without financials. Our financial statement spreader is available to add additional insight when available.

Outcome-based training: Models are trained on real-world events like bankruptcies and payment deterioration, not just proxy variables.

Our Measurements

We evaluate models over a 12-month probability of default (PD) window using industry-standard metrics:

AUC (Area Under the Curve): Measures how well the model separates low-risk vs. high-risk accounts. Our AUC: ~0.85 vs. ~0.70–0.83 benchmarks

False Positives (Type II Error). Measures how often safe accounts are incorrectly flagged as risky. Our model produces fewer false positives than benchmarks.

Confidence Indicators

Our models prioritize the most predictive data available. In some cases, data may be limited. When that happens, scores may include confidence indicators to help you understand how much data supports the prediction.

As with any model:

Scores are directional, not absolute

They improve decision consistency across your team

They reduce reliance on gut feel and manual research

Scout, Our AI Assistant

When in doubt, ask Scout. Need more context on a score? Use Scout, our AI-powered assistant, to break down:

Why a score changed

What data is driving risk

How to interpret a specific company

Click the ✨ icon next to any score or start a chat in the bottom right corner.

Questions? Email support@creditpulse.com for support.